Expense Reimbursement – Business Travel and Subsistence

Travel costs incurred wholly, exclusively, and necessarily for business purposes may be reimbursed by a company and are typically not subject to tax.

Qualifying business travel includes:

- Trips to visit clients or suppliers

- Travel to temporary workplaces

- Attendance at business-related conferences or training events

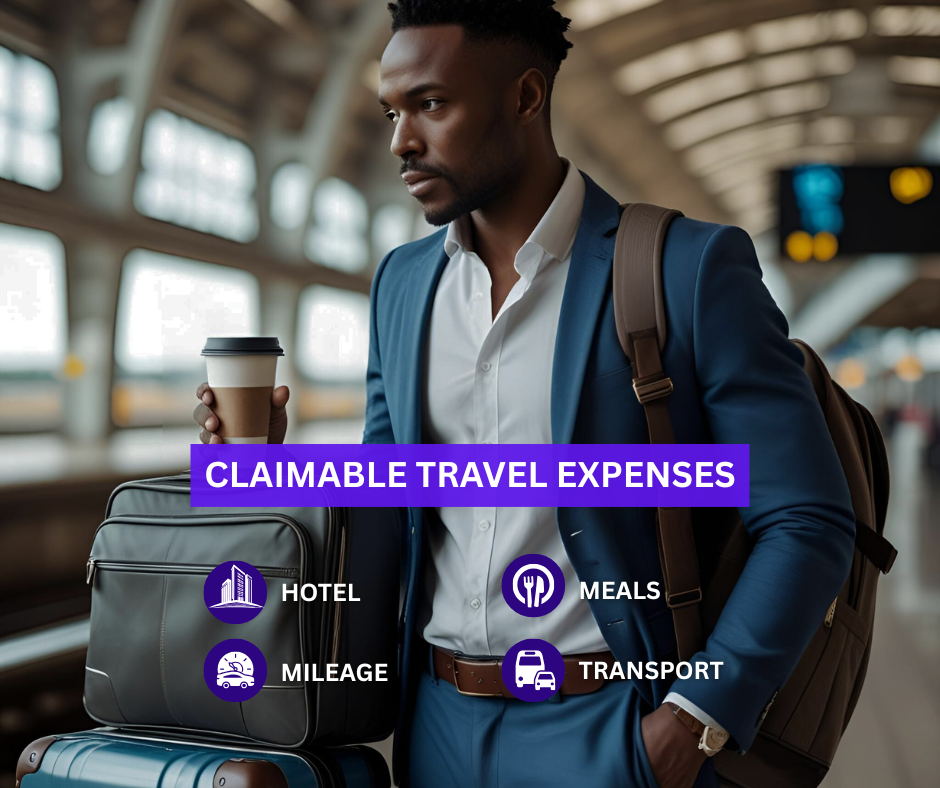

Reimbursable expenses may include:

- Public transport fares (train, bus, taxi, flight)

- Car mileage using HMRC’s approved rates:

– 45p per mile for the first 10,000 business miles

– 25p per mile thereafter - Hotel stays when overnight travel is required

- Meals and reasonable subsistence while away from the regular workplace

Travel between home and a permanent workplace is considered ordinary commuting and is not eligible. A temporary workplace, in HMRC terms, is one where work is carried out for less than 24 months or is not the usual place of employment.

Clear records such as mileage logs, tickets, and receipts must be maintained for all reimbursed expenses.